miércoles, 27 de febrero de 2013

Signals For Europe, Few Options in a Vicious Cycle of Debt

Signals For Europe, Few Options in a Vicious Cycle of Debt Europe has a $1 trillion problem. As difficult as the last two years have been for Europe, 2012 could be even tougher. Each week, countries will need to sell billions of dollars of bonds - a staggering $1 trillion in total - to replace existing debt and cover their current budget deficits. At any point, should banks, pensions and other big investors balk, anxiety could course through the markets, making government officials feel like they are stuck in a scary financial remake of 'Groundhog Day.' Even if governments attract investors at reasonable interest rates one month, they will have to repeat the process again the next month - and signs of skittish buyers could make each sale harder to manage than the previous one. 'The headline risk is enormous,' said Nick Firoozye, chief European rates strategist at Nomura International in London. Given this vicious cycle, policy makers and investors are closely watching the debt auctions for potential weakness. On Thursday, Spain is set to sell as much as 5 billion euros ($6.3 billion) of government bonds. Italy follows on Friday with an auction of more than $9 billion. The current challenge for Europe is to keep Italy and Spain from ending up like Greece and Portugal, whose borrowing costs rose so high last year that it signaled real likelihood of default, making it impossible for the governments to find buyers for their debt. Since then, Greece and Portugal have been reliant on the financial backing of the European Union and the International Monetary Fund. The intense focus on the sovereign debt auctions - and their importance to the broader economy - starkly underscores the difference between European and American responses to their crises. Since 2008, there has been almost no private sector interest to buy new United States residential mortgage loans, the financial asset at the root of the country's crisis. To make up for that lack of investor demand, the federal government has bought and guaranteed hundreds of billions of dollars of new mortgages. In Europe, policy makers are still expecting private sector buyers to acquire the majority of government debt. Last month, in perhaps the boldest move of the crisis, the European Central Bank lent $620 billion to banks for up to three years at a rate of 1 percent. Some officials had hoped that these cheap loans would spur demand for government debt. The idea is that financial institutions would be able to make a tidy profit by borrowing from the central bank at 1 percent and using the money to buy government bonds that have a higher yield, like Spain's 10-year bond at 5.5 percent. But the sovereign debt markets continue to show signs of stress. Italy's 10-year government bond has fallen in price, lifting its yield to more than 7 percent, a level that shows investors remain worried about the financial strength of Italy's government. And European banks appear to be hoarding much of the money they borrowed from the central bank, rather than lending it to governments. Money deposited by banks at the European Central Bank, where it remains idle, stands at $617 billion, up from $425 billion just a month ago. 'It's hard to see why a banker would want to tie up money in a European sovereign for, say, three years,' said Phillip L. Swagel at the University of Maryland's School of Public Policy, who served as assistant secretary for economic policy under Treasury Secretary Henry M. Paulson Jr. Italy's troubles highlight how hard it is to generate demand for a deluge of new debt from a dwindling pool of investors. The country needs to issue as much as $305 billion of debt this year, the highest in the euro zone. By comparison, France, with the second highest total, needs to auction $243 billion of new debt, according to estimates by Nomura. Governments like Italy's are at the mercy of markets because they simply don't have the cash to pay off even some of their bonds that come due. They must issue new bonds to cover their old debts, as well as their budget deficits, at a time when investors are growing scarce. Banks, traditionally big holders of government bonds, have been selling Italian debt. 'We've seen a lot of liquidation by non-European investors,' said Laurent Fransolet, head of European interest rate strategy at Barclays Capital in London. For instance, Nomura Holdings in Japan slashed its Italian debt holdings, mostly government bonds, to $467 million on Nov. 24, from $2.8 billion at the end of Sept. European banks have also been dumping the debt. BNP Paribas, a French bank, cut its exposure to Italian government bonds to $15.5 billion at the end of October, from $26 billion at the end of June. Italian banks, though large owners of their government's obligations, may not want to take on too much more, to keep their investors happy. Shares in UniCredit have fallen more than 40 percent since last week as the Italian firm has tried to raise capital to comply with new regulations. There are ways to avoid spectacularly bad debt auctions, at least in the short term. The central bank can help by buying a country's bonds in the market ahead of a new debt sale. That would help bolster prices at the auction, or at least keep them stable. There is also some evidence that banks' government-bond selling may have abated at the end of last year, according to Mr. Fransolet. Central bank figures show European financial firms acquired $2.4 billion of Spanish government bonds in November, after selling a monthly average of $4.8 billion in the preceding three months. Governments may also be able to attract new buyers to their bond markets. Belgium sold $7.2 billion of government bonds to local retail investors last month, in part appealing to their patriotism. Opportunistic hedge funds, betting the market is too pessimistic about certain European countries, may also bite. Saba Capital Management, a New York-based hedge fund headed by the former Deutsche Bank trader Boaz Weinstein, owns Italian government bonds, though it does so as part of a wider trading strategy that includes bets that could pay off if Europe's problems worsen. But it is doubtful that Italy and Spain can find enough new buyers this year to bring their bond yields down to sustainable levels. Instead, if their economies slow - and if their governments become unpopular - debt auctions could fail and their cost of borrowing could rise even more. All eyes would then turn to the central bank for drastic action. It could lend more cheap money to banks, in the hope that some of it might find its way into government bonds. Or it could become a big buyer of government bonds itself, printing euros to finance the purchases. But that may not be a lasting solution, since the central bank's actions could scare off private investors. Typically, when government-backed organizations like the central bank hold a country's debt, their claims on the debtor rank higher than those of other creditors. For that reason, private investors might think their holdings would fall in value if the central bank became a big owner of Italian debt - and they might retreat. At the same time, the crisis response in the United States did not depend solely on government-backed entities like the Federal Reserve to buy housing loans. Professor Swagel of the University of Maryland points out that banks and investors also took large losses on existing housing debt. While painful, the mortgage debt proved less of a drag on the financial system. So far, Europe has been averse to taking permanent losses on government bonds. Except in the case of Greek debt, European policy makers have shied away from any plan that could mean private holders of government debt get hurt. However, Nouriel Roubini, a professor of economics at the Stern School of Business at New York University, recently argued in a Financial Times editorial that Italy's debt should be reduced to 90 percent of the gross domestic product from 120 percent. In such a situation, investors might suffer a 25 percent hit on the value of their Italian bonds, he said. Such haircuts might seem like the recipe for more instability right now. But if Europe struggles to find buyers for its debt, more radical options are likely to be considered. Europe's debt problem is huge, and the experience in the United States suggests dealing with it may take several, more drastic approaches. 'If you go halfway, you'll never get to the end,' Professor Swagel said. 'And that describes European policy-making.'

martes, 12 de febrero de 2013

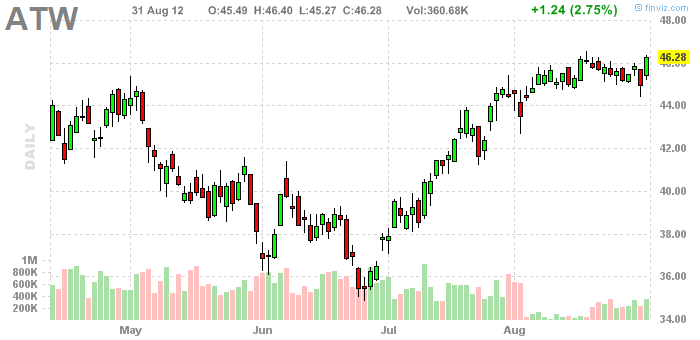

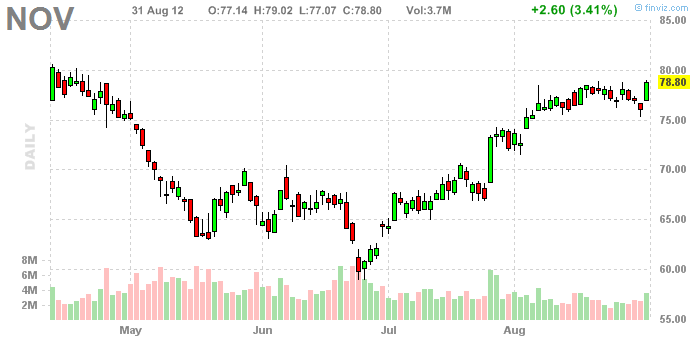

Signals Swing trading opportunities

Signals

Several stocks are breaking out and there are some nice setups showing up in our scans. Many stocks are going sideways during market consolidation and are now breaking out.

lunes, 11 de febrero de 2013

Forex Weidmann-Bundesbank profit will be crimped by reserves

Forex Weidmann-Bundesbank profit will be crimped by reserves BERLIN (Reuters) - The Bundesbank profit turned over to the federal government will be considerably smaller this year than in 2011 due to the risk provisions linked to the euro zone crisis, central bank president Jens Weidmann was quoted telling Der Spiegel. Weidmann said the German central bank had to raise its reserves due to the greater risks and had consulted with its accountants. In 2012 the Bundesbank had a 2.2 billion euro profit and set aside 1.6 billion for risks. 'The distributed profit will be considerably less than last year,' Weidmann said, without providing any specific numbers. Weidmann also said that he had doubts whether European central banks will be able to make a profit on Greek sovereign bonds that euro zone countries are eager to use as part of the latest Greek bailout. 'It's assumed that the central banks will earn a profit from purchasing the bonds. But that is not certain at all. On the contrary, the balance sheet risks have increased. And that affects not only the Greek bonds but also all the extraordinary monetary measures related to the crisis.' (Reporting By Erik Kirschbaum; Editing by Elaine Hardcastle)

martes, 5 de febrero de 2013

Oil Consumer Comfort Highest in Six Months

Oil Consumer Comfort Highest in Six Months Consumer confidence in the U.S. last week reached the highest level since July as the improving job market helped allay pessimism. The Bloomberg Consumer Comfort Index was minus 44.7 in the period ended Jan. 8 from minus 44.8 the prior week. As recently as October, the index registered its lowest readings since the 2007-2009 recession, making 2011 the second-worst year in 25 years of data. It's since increased in four of the past five weeks. 'Considering where it's been, the trend is a welcome one,' Gary Langer, president of Langer Research Associates LLC in New York, which compiles the index for Bloomberg, said in a statement. 'Sentiment is hardly on a predictable path, given factors including the uncertainty of the 2012 presidential election, volatility in global markets and economic question marks from Europe to China.' Less unemployment and growing payrolls may be lifting consumers' moods, providing the spark for increases in consumer spending, which accounts for about 70 percent of the economy. Nonetheless, gasoline prices that are once again rising and wage gains that fail to keep pace with inflation may be obstacles to greater improvement in confidence. Other reports today showed retail sales rose less than forecast in December and claims for jobless benefits climbed more than projected in the first week of the year. Retail Sales Purchases increased 0.1 percent last month after a 0.4 percent advance in November that was more than initially reported, Commerce Department figures showed. Economists forecast a 0.3 percent December rise, according to the median estimate in a Bloomberg News survey. Purchases excluding automobiles fell 0.2 percent, the first decline since May 2010. The number of applications for unemployment benefits climbed by 24,000 to 399,000 in the week ended Jan. 7, Labor Department figures showed. The median forecast of 46 economists in a Bloomberg survey projected 375,000. Stocks rose as sales of government securities in Spain and Italy eased concern the countries would struggle to finance their debts. The Standard & Poor's 500 Index climbed 0.1 percent to 1,293.76 at 9:40 a.m. in New York. The comfort survey's gauge of Americans' views of the current state of the economy rose to minus 82.1 last week from minus 82.9 in the prior period. The buying climate index held at minus 49.4, and the measure of personal finances decreased to minus 2.6 from minus 2.2. The gain in the cumulative Bloomberg index last week was within the survey's three-point margin of error. More Jobs Better employment opportunities are probably holding up confidence. Payrolls increased by 200,000 in December, and the jobless rate dropped to 8.5 percent, the lowest since February 2009, a Labor Department report showed last week. Employers added 1.64 million workers in 2011, surpassing the prior year's 940,000 advance and the biggest gain since 2006. Sentiment has been improving among lower-income Americans. The index for those earning less than $15,000 per year increased to the highest level since October, and those making up to $24,999 were the most optimistic since February. The ebbing of pessimism was also evident among older households. The measure of confidence among those older than 65 rose to minus 39.9, the best reading since April. Brighter moods may help drive consumer spending in 2012 following the holiday shopping season. 'Extremely Pleased' 'We are extremely pleased with our December sales results as we significantly exceeded our expectations,' Sherry Lang, a spokeswoman for TJX Cos. said in Jan. 5 conference call. Sales at the Framingham, Massachusetts-based retailer increased 8 percent last month. 'Further, we entered January with very lean inventories and the flexibility to ship fresh merchandise at great values to our stores.' The gain in the Bloomberg index parallels improvement in other surveys. The Conference Board's confidence gauge increased in December to the highest level since April. That same month the Thomson Reuters/University of Michigan index of consumer confidence rose to the highest level since June. Nonetheless, rising gasoline prices may constrain sentiment. The cost of a regular gallon of fuel at the pump climbed to $3.38 yesterday, up 5.5 percent from a 10-month low reached on Dec. 20, according to data from AAA, the nation's largest auto group. 'While the recent trend in consumer confidence is encouraging, risks remain,' said Joseph Brusuelas, a senior economist at Bloomberg LP in New York. 'The recent rise in gasoline prices is likely to act as a restraint on improving consumer confidence in January.' Annual Averages Bloomberg's comfort index, which began in December 1985, averaged minus 46.8 for all of last year, second only to 2009's minus 47.9 as the worst year on record. The gauge averaged minus 45.7 for 2010. The Consumer Comfort Index is based on responses to telephone interviews with a random sample of 1,000 consumers 18 years old and over. Each week, 250 respondents are asked for their views on the economy, personal finances and buying climate; the percentage of negative responses for each measure is subtracted from the share of positive views. The results are then summed and divided by three. The most recent reading is based on the average of responses over the previous four weeks. The comfort index can range from 100, indicating every participant in the survey had a positive response to all three components, to minus 100, signaling all views were negative. Field work for the index is done by SSRS/Social Science Research Solutions in Media, Pennsylvania. To contact the reporter on this story: Alex Kowalski in Washington at akowalski13@bloomberg.net To contact the editor responsible for this story: Christopher Wellisz at cwellisz@bloomberg.net

Forex Europe hit by downgrade speculation

Forex ROME (AP) -- Europe's ability to fight off its debt crisis was again thrown into doubt Friday when the euro hit its lowest level in over a year and borrowing costs rose on expectations that the debt of several countries would be downgraded by rating agency Standard & Poor's. Stock markets in Europe and the U.S. plunged late Friday when reports of an imminent downgrade first appeared and the euro fell to a 17-month low. The fears of a downgrade brought a sour end to a mildly encouraging week for Europe's heavily indebted nations and were a stark reminder that the 17-country eurozone's debt crisis is far from over. Earlier Friday, Italy had capped a strong week for government debt auctions, seeing its borrowing costs drop for a second day in a row as it successfully raised as much as €4.75 billion ($6.05 billion). Spain and Italy completed successful bond auctions on Thursday, and European Central Bank president Mario Draghi noted 'tentative signs of stabilization' in the region's economy. A credit downgrade would escalate the threats to Europe's fragile financial system, as the costs at which the affected countries — some of which are already struggling with heavy debt loads and low growth — could borrow money would be driven even higher. The downgrade could drive up the cost of European government debt as investors demand more compensation for holding bonds deemed to be riskier than they had been. Higher borrowing costs would put more financial pressure on countries already contending with heavy debt burdens. In Greece, negotiations Friday to get investors to take a voluntary cut on their Greek bond holdings appeared close to collapse, raising the specter of a potentially disastrous default by the country that kicked off Europe's financial troubles more than two years ago. The deal, known as the Private Sector Involvement, aims to reduce Greece's debt by €100 billion ($127.8 billion) by swapping private creditors' bonds with new ones with a lower value, and is a key part of a €130 billion ($166 billion) international bailout. Without it, the country could suffer a catastrophic bankruptcy that would send shock waves through the global economy. Prime Minister Lucas Papademos and Finance Minister Evangelos Venizelos met on Thursday and Friday with representatives of the Institute of International Finance, a global body representing the private bondholders. Finance ministry officials from the eurozone also met in Brussels Thursday night. 'Unfortunately, despite the efforts of Greece's leadership, the proposal put forward ... which involves an unprecedented 50 percent nominal reduction of Greece's sovereign bonds in private investors' hands and up to €100 billion of debt forgiveness — has not produced a constructive consolidated response by all parties, consistent with a voluntary exchange of Greek sovereign debt,' the IIF said in a statement. 'Under the circumstances, discussions with Greece and the official sector are paused for reflection on the benefits of a voluntary approach,' it said. Friday's Italian auction saw investors demanding an interest rate of 4.83 percent to lend Italy three-year money, down from an average rate of 5.62 percent in the previous auction and far lower than the 7.89 percent in November, when the country's financial crisis was most acute. While Italy paid a slightly higher rate for bonds maturing in 2018, which were also sold in Friday's auction, demand was between 1.2 percent and 2.2 percent higher than what was on offer. The results were not as strong as those of bond auctions the previous day, when Italy raised €12 billion ($15 billion) and Spain saw huge demand for its own debt sale. 'Overall, it underscores that while all the auctions in the eurozone have been battle victories, the war is a long way from being resolved (either way),' said Marc Ostwald, strategist at Monument Securities. 'These euro area auctions will continue to present themselves as market risk events for a very protracted period.' Italy's €1.9 trillion ($2.42 trillion) in government debt and heavy borrowing needs this year have made it a focal point of the European debt crisis. Italy has passed austerity measures and is on a structural reform course that Premier Mario Monti claims should bring down Italy's high bond yields, which he says are no longer warranted. Analysts have said the successful recent bond auctions were at least in part the work of the ECB, which has inundated banks with cheap loans, giving them ready cash that at least some appear to be using to buy higher-yielding short-term government bonds. Some 523 banks took €489 billion in credit for up to three years at a current interest cost of 1 percent.

Suscribirse a:

Entradas (Atom)